It’s no secret that I question whether the interests of VCs and founders are properly aligned with each other in many venture capital deals. I’m not trying to be snarky or controversial. There is a fundamental, structural explanation for why VCs’ and startup founders’ interests often diverge.

When I talk about a misalignment of interests, I’m not talking about nefarious people acting in bad faith. There are many talented venture investors out there working tirelessly to do right by founders and bring new technologies to the market. However, the venture capital industry has evolved in a way that makes the fundamental incentives at work for VCs and founders difficult to align. No one is trying to do wrong by anyone. Everyone — VCs and founders alike — is just doing their best to do what the market is telling them to do. But the market has very different incentives for investors than for founders. And this divergence has grown sharper over time.

Let me explain.

Venture firms, like other private equity investment firms, run on what’s known as a 2/20 model. VCs are compensated in part (the 2%) by fees on their total assets under management (AUM), and in part by the profits on their investments (the 20%).

There are some interesting tensions between the two incentives at work in the 2/20 model. These tensions often go unnoticed. On the one hand, VCs are incentivized to grow their AUM to increase their management fees. On the other, they are rewarded via carried interest for the performance of their investments. Carried interest is supposed to provide the most powerful incentive to VCs in the 2/20 model. But management fees accumulate a lot faster than carry — it can take 10 years or more for an early-stage investment to mature — so VCs face strong financial pressures to build up their AUM and fund sizes.

Investors face social and status pressures as well. Bigger venture funds mean more industry recognition for VCs, more media coverage of their funds, and more attention to their portfolio companies and market views.

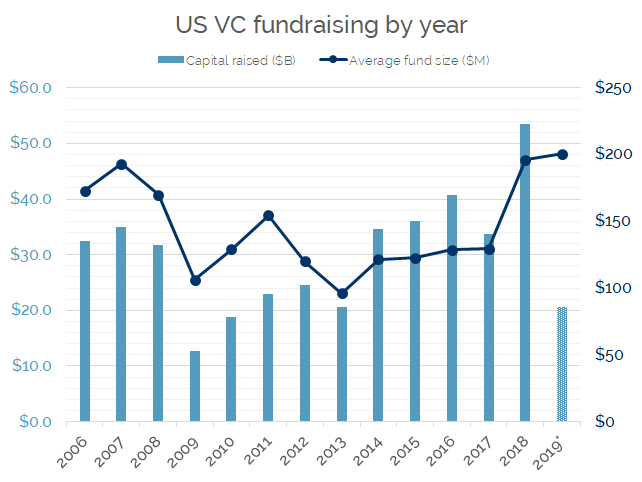

So it’s not surprising to see fund sizes grow rapidly with rising markets and more attention to the VC industry from non-traditional players looking for opportunities for yield in the most recent market cycle. Right now, we are seeing the highest average fund size in venture capital history. Today, 66% of all U.S. venture dollars in are in funds of $500 million or more, and 13 of the 15 largest-ever venture funds have been raised since 2015.

So What’s the Problem?

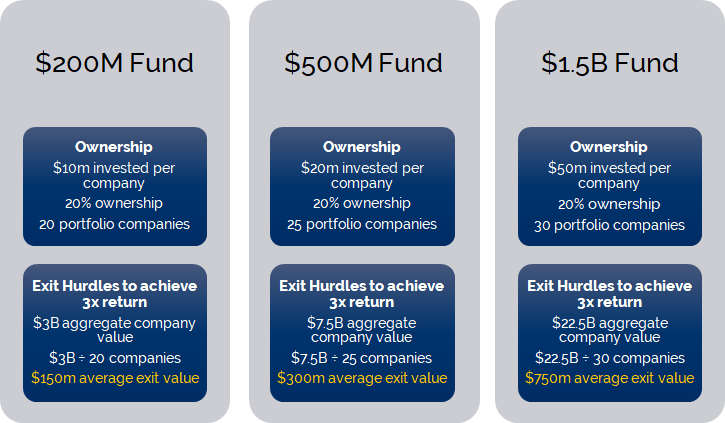

As it turns out, the bigger the fund, the harder it is to generate great returns for investors. Without diving too deeply into the math at the moment — we can do that another time — there’s a rule of thumb for how venture funds deliver 3x gross returns to their investors. The average exit value of a venture fund’s portfolio companies generally needs to be at least half the total size of the fund. In other words, for those 66% of venture dollars in funds of $500 million or more, the exit values of their portfolio companies need to average at least $250 million. This average includes all the companies in each VC fund with values that will go to zero.

But average exit values for VC-backed companies are not above $250 million. In fact, data from Pitchbook and the National Venture Capital Association show that median exit values in the past 5 years have ranged between $60 and $85 million. So venture firms are incentivized to create ever-larger outliers, those unicorns and decacorns that can push their averages up into solid 3x return territory, to make up for the fact that the median exit value is so much lower than the average they need.

Most of those aspiring unicorns will not succeed. You know that. The VCs know that, too. But the incentives for VCs encourage them to keep pressing for those big wins, because $100 million exits will not move their funds toward their targets. From the perspective of fund economics, it is better for portfolio companies to swing for the fences or die trying. After all, there’s a whole portfolio full of chances — in larger VC funds, 30 or more — and who knows which ones will hit?

If you’re the founder of an early-stage company, you don’t have a portfolio of chances. There’s only one shot. Your median exit is not likely to be $1 billion or even $250 million. Instead, it’s likely to average about $80 million — assuming your company survives to exit. From a founder’s perspective, is it worth all of your sacrifices and years of hard work to “go big or go home?” Do you want to turn down a $100 million offer that sets you up for life and rewards your years of work because it didn’t move the needle for investors?

As a founder, you get to make fundamental choices about the nature of the game you are playing as you grow your company. How much you choose to raise — and how your choices align with your investors’ incentives — has a huge influence on your odds of winning.